How to Make a Strong Offer on a House in a Competitive Market

In today's Mid-Michigan real estate market, well-priced homes in desirable neighborhoods across Genesee, Oakland, and Livingston Counties are drawing multiple offers. Buyers are discovering that the old strategy of simply offering list price doesn't always win the day. After more than 20 years in the real estate industry, I've helped buyers navigate competitive situations successfully — and the winning formula takes more than just a high number. It takes strategy, preparation, and a clear understanding of what actually motivates sellers.

Understand What Sellers Really Want

Before diving into tactics, it helps to understand what's driving a seller's decision when they receive multiple offers. Price matters, of course, but sellers also care deeply about:

- Certainty of closing: A slightly lower offer from a well-qualified buyer is often more attractive than a higher offer from someone whose financing is shaky. Sellers want confidence that the deal will make it to the closing table.

- Timeline flexibility: Sellers have their own move plans — finding a new home, coordinating a move, closing on their next purchase. An offer that aligns with their timeline is inherently more valuable.

- Minimal hassle: Sellers prefer clean, straightforward offers with fewer contingencies and less risk of renegotiation. An offer that feels simple and reliable stands out.

Keeping these priorities in mind will help you craft an offer that's strategically competitive, not just financially aggressive.

Get Fully Pre-Approved — Not Just Pre-Qualified

This is the single most important step you can take before writing an offer. There's a significant difference between pre-qualification and pre-approval, and sellers and their agents know it.

Pre-qualification is a quick conversation with a lender where they estimate what you might be able to borrow. Pre-approval means the lender has pulled your credit, verified your income and assets, and issued a commitment letter. When I present an offer to a listing agent, a fully underwritten pre-approval letter carries dramatically more weight than a pre-qualification letter. It tells the seller that your financing is solid and the deal is far less likely to fall apart.

In competitive situations, I sometimes recommend going a step further with an underwriting pre-approval, where the lender has cleared most conditions before you even have a property under contract. It takes extra work upfront, but it gives you a serious advantage. For more on the buyer's side of the process, see our first-time buyer's guide.

Use an Escalation Clause — When It Makes Sense

An escalation clause is a provision in your offer that automatically increases your bid by a specified amount above any competing offer, up to a maximum price you set. For example, you might offer $275,000 with an escalation clause that beats any competing offer by $2,000, up to a cap of $285,000.

Escalation clauses can be effective, but they come with trade-offs:

- Pros: They show serious intent and can ensure you don't lose a home over a small price gap. They also create transparency — you know exactly what your ceiling is.

- Cons: They reveal your maximum price to the seller, which eliminates some negotiation leverage. They can also feel impersonal and may not be appropriate in every situation.

I use escalation clauses selectively. In some competitive Mid-Michigan markets, they work well for move-up buyers who have a clear budget and want to secure a specific home. In other situations, a strong but straightforward offer with clean terms outperforms an escalation clause. The key is knowing your market and your competition — and that's where a knowledgeable local agent makes all the difference.

Increase Your Earnest Money Deposit

Earnest money is your good-faith deposit that shows the seller you're serious. A standard deposit in many markets is 1% of the purchase price, but in competitive situations, offering a higher earnest money deposit — 2% or even 3% — signals commitment and financial strength.

Just make sure you understand the terms under which you'd get the deposit back if the deal doesn't close. The deposit should be held in escrow by a title company, and the contingencies in your contract should clearly outline the conditions for a refund. I always make sure my clients understand this before we submit. For context on how earnest money fits into the broader closing process, see our guide to what to expect at closing.

Offer Flexible Closing Dates

One of the most underrated negotiation strategies is flexibility on timing. Many buyers fixate on their own timeline, but the sellers may have entirely different priorities. Some sellers need a quick close. Others need 60 or 90 days to find their next home and coordinate a move. Still others have already purchased a new place and need to sell quickly to avoid carrying two mortgages.

When I write an offer, I ask the listing agent what timeline the seller prefers. If we can align our closing date with theirs — or even offer them post-closing occupancy for a few days — it can make our offer significantly more attractive without costing my client a single dollar.

In areas like Grand Blanc, Fenton, and Brighton, where many sellers are also buyers, this flexibility can be the tiebreaker between two otherwise equal offers.

Consider Appraisal Gap Coverage

In a competitive market, buyers sometimes offer above the likely appraised value of a home to win. But here's the catch: if the home appraises below your offer price, your lender will only loan based on the appraised value — not the contract price. That gap becomes your responsibility.

Appraisal gap coverage is a provision in your offer where you agree to cover some or all of the difference between the appraised value and your offer price, up to a specified cap. For example, you might offer $300,000 with appraisal gap coverage up to $10,000 — meaning if the home appraises at $290,000, you'd cover the $10,000 difference out of pocket.

This strategy signals serious financial commitment and can be a powerful differentiator. However, it requires careful thought:

- Only commit to an amount you genuinely have available in cash above your down payment.

- Set a reasonable cap that protects you from overpaying significantly.

- Understand that you're taking on risk — if the home appraises well below your offer, you may be paying more than the property is worth.

I help my buyers evaluate appraisal gap coverage on a case-by-case basis, weighing the property's likely value, the competitive landscape, and the buyer's financial comfort zone. Our guide to what happens when a home appraises below offer price covers all the options if an appraisal comes in low.

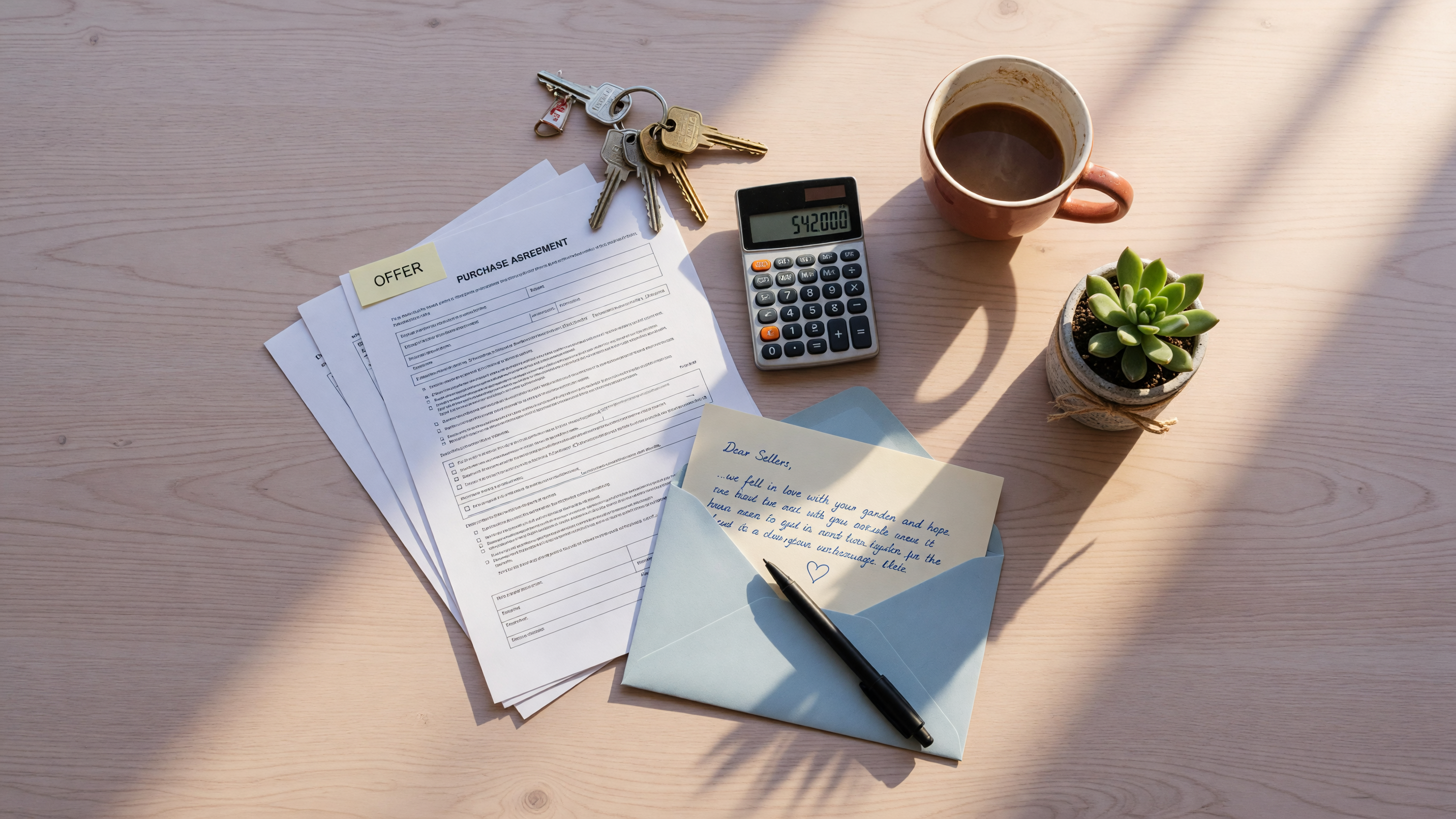

Write a Personal Letter — When It's Genuine

A personal letter to the seller can add a human element to your offer that purely financial terms can't match. Sellers who have lived in their home for years — who raised their kids there, who put real love into the garden — sometimes care deeply about who comes next.

But I'll be honest: personal letters are only effective when they're genuine. A form letter that could be written by anyone won't move the needle. The best letters are specific. They mention something about the home that resonates with you personally. They share who you are and why this particular house, on this particular street, feels like home.

It's worth noting that the Michigan Association of REALTORS® recommends fair housing compliance when writing buyer letters, and some states have moved to restrict them. I help my clients navigate this carefully so their letter is heartfelt and appropriate without creating any legal concerns.

Use a Pre-Inspection Strategy

In a competitive market, inspection contingencies can feel like a liability. Sellers worry that a buyer will use the inspection to renegotiate the price or back out entirely. So some buyers consider waiving the inspection altogether. I strongly advise against that. What I recommend instead is a pre-inspection strategy.

Here's how it works: before you make an offer, you schedule a pre-inspection of the property. This gives you a clear picture of the home's condition before you commit. With that knowledge, you can write a stronger offer — either with a limited inspection contingency (covering only major structural, mechanical, or safety issues) or with the inspection completed and any known issues already factored into your offer price.

Pre-inspections aren't always possible — especially in fast-moving markets where homes sell in days. But when the opportunity exists, they give you a significant advantage. For more on what inspectors look for, see our home inspections 101 guide.

Know When to Walk Away

Competitive doesn't always mean desperate. The strongest offer is one you can live with — financially and emotionally. Here are signs it might be time to step back:

- The escalation clause takes you beyond your true budget ceiling.

- You're being asked to waive contingencies that protect your financial security.

- The home has known issues that you can't comfortably absorb.

- The bidding has pushed the price well above comparable sales in the area.

- You're making emotional decisions instead of strategic ones.

Walking away from a home you love is never easy, but it's sometimes the smartest move. Overpaying for a home or skipping essential protections can create financial stress that lasts far longer than the disappointment of losing one listing. There will always be another house — and the right one will come along when the terms are right. Our guide to contingencies explains what protections you should never give up.

Ready to Make Your Move?

Buying a home in a competitive market is challenging, but with the right strategy, it's absolutely achievable. I've helped buyers across Mid-Michigan win in competitive situations by combining preparation, smart strategy, and steady guidance. If you're ready to make your move, schedule a consultation or call me at 810-513-3335.

Keller Williams First · 810-513-3335 · Schedule a consultation